Reports on three studies below with pdfs attached and a report below by a very large life insurance company on excess deaths. A link to a review of the 3rd study is down below also.

Aloha,

Bud

- Summarized by Nicolas Hulscher, MPH @NicHulscher

Epidemiologist and Administrator at the McCullough Foundation (@mcculloughfund)

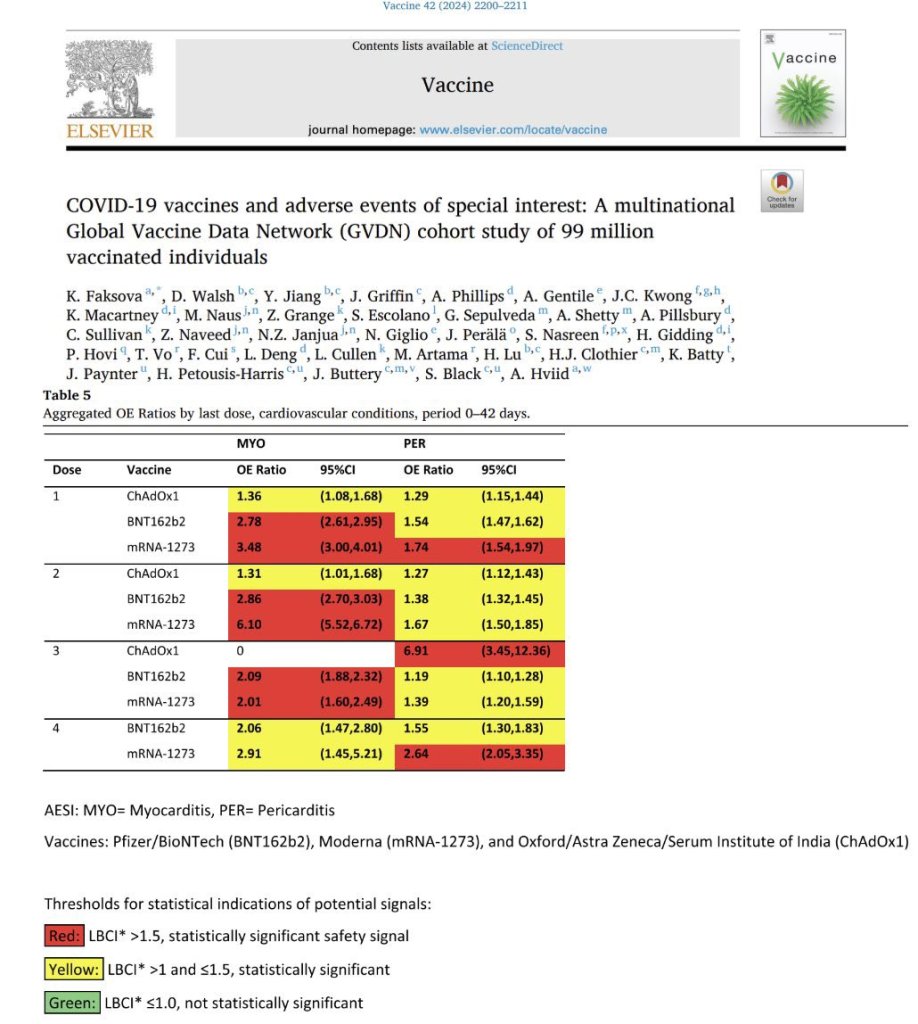

https://thefocalpoints.com This study aimed to evaluate the risk of adverse events of special interest (AESI) following COVID-19 vaccination from 10 sites across eight countries.

The largest COVID-19 “vaccine” safety study ever conducted, involving 99 million individuals, confirmed that the injections are NOT SAFE FOR HUMAN USE:

➊ 610% increased risk of myocarditis following mRNA platform injection.

➋ 378% increased risk of acute disseminated encephalomyelitis (ADEM) following mRNA injection.

➌ 323% increased risk of cerebral venous sinus thrombosis (CVST) following viral-vector injection.

➍ 249% increased risk of Guillain-Barré syndrome (GBS) following viral-vector injection.

https://www.sciencedirect.com/science/article/pii/S0264410X24001270?via%3Dihub and attached as pdf

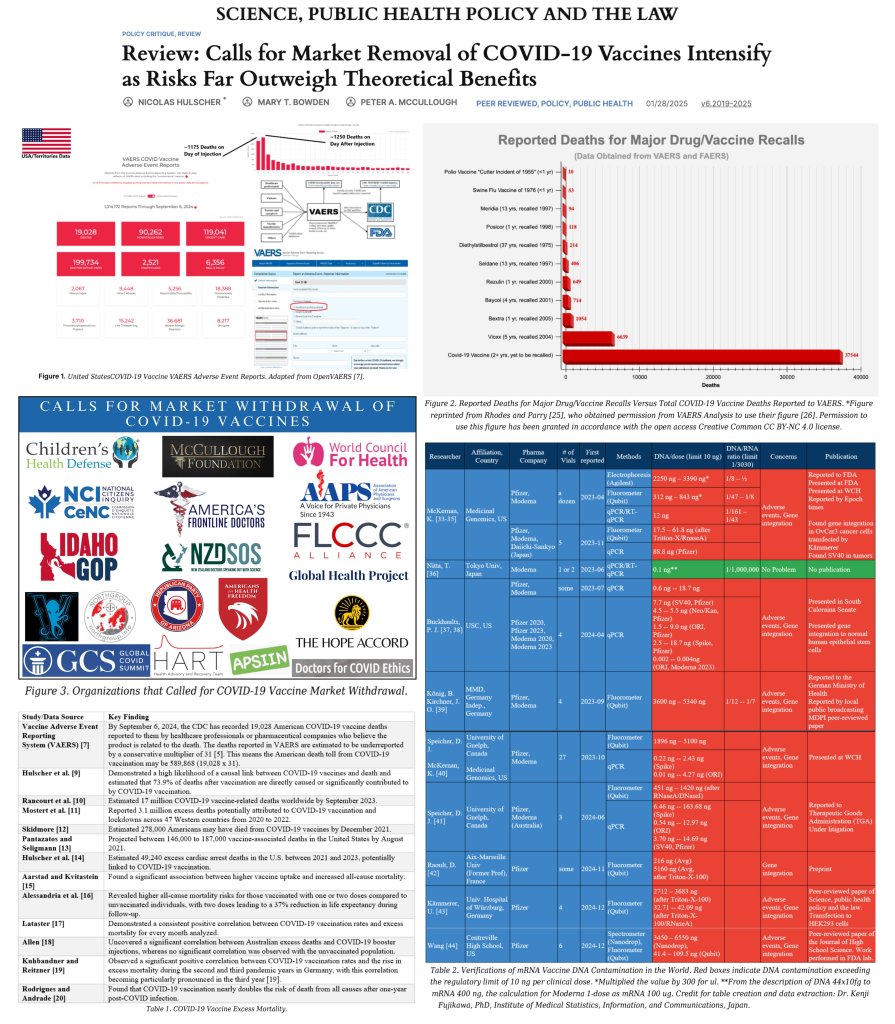

- “Review: Calls for Market Removal of COVID-19 Vaccines Intensify as Risks Far Outweigh Theoretical Benefits”

- Widespread & Unified Calls for Market Withdrawal – More than 81,000 physicians, scientists, and concerned citizens, 240 elected officials, 17 public health & physician organizations, 2 State Republican Parties, 17 GOP County Committees, and 6 global studies demand immediate removal.

- Excess Mortality – 12 studies and VAERS confirm mass COVID-19 ‘vaccination’ led to a catastrophic number deaths — up to 17 million.

- FDA Class I Recall Indicated – 37,544 VAERS-reported deaths exceed past vaccine recall limits by up to 375,340%.

- Negative Efficacy – 6 studies have demonstrated that COVID-19 ‘vaccination’ increases your risk of SARS-CoV-2 infection.

- DNA Contamination – 11 reports have found DNA contamination in COVID-19 vaccines, documented across multiple manufacturers, vaccine platforms, and geographic regions, with levels exceeding regulatory thresholds by up to 65,500%. Please share this study far and wide so we can finally put an end to the catastrophic COVID-19 “vaccination” program and initiate the justice phase of the pandemic.

Summarized above by @P_McCulloughMD, @McCulloughFund, @MdBreathe

The Study Showing the mRNA Vaccine Cancer Link That They Don’t Want You to See (study attached pdf)

Review by Rebekah Barnett at the link immediately above of the study. 19 March 2025 1:00 PM

Company cites “non-pandemic-related morbidity” and “unusual claims adjustments” in explanation of losses from group life insurance business: Stock falling, replaces CEO

Jun 15, 2022

Five months after breaking the story of the CEO of One America insurance company saying deaths among working people ages 18-64 were up 40% in the third quarter of 2021, I can report that a much larger life insurance company, Lincoln National, reported a 163% increase in death benefits paid out under its group life insurance policies in 2021.

This is according to the annual statements filed with state insurance departments — statements that were provided exclusively to Crossroads Report in response to public records requests.

The reports show a more extreme situation than the 40% increase in deaths in the third quarter of 2021 that was cited in late December by One America CEO Scott Davison — an increase that he said was industry-wide and that he described at the time as “unheard of” and “huge, huge numbers” and the highest death rates that have ever been seen in the history of the life insurance business.

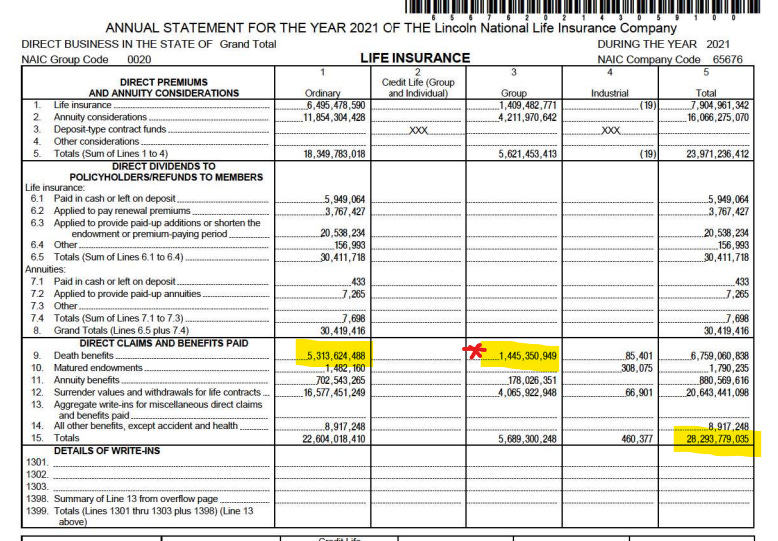

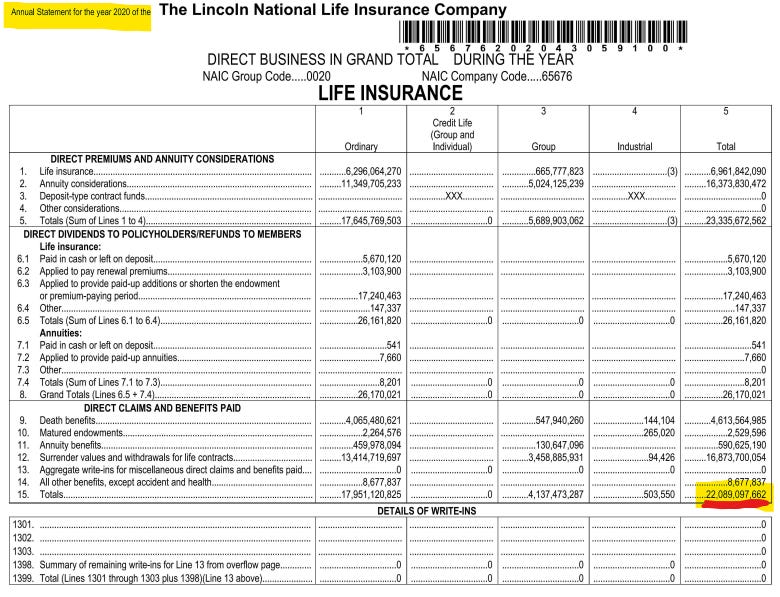

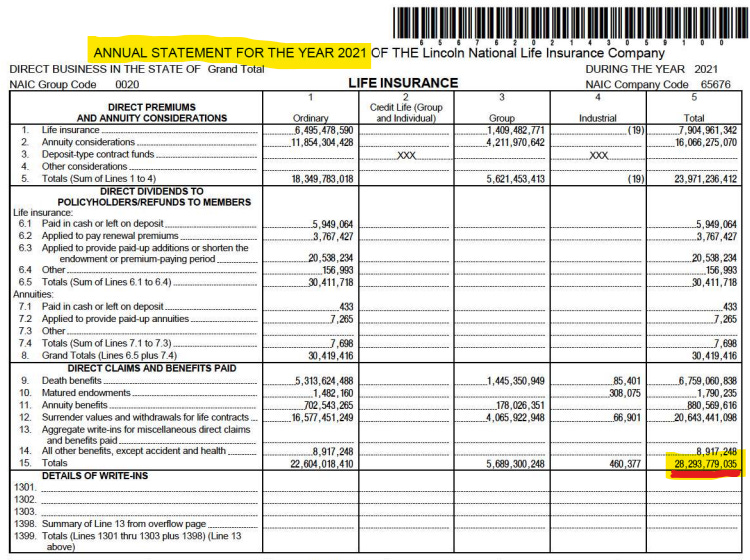

The annual statements for Lincoln National Life Insurance Company show that the company paid out in death benefits under group life insurance polices a little over $500 million in 2019, about $548 million in 2020, and a stunning $1.4 billion in 2021.

From 2019, the last normal year before the pandemic, to 2020, the year of the Covid-19 virus, there was an increase in group death benefits paid out of only 9 percent. But group death benefits in 2021, the year the vaccine was introduced, increased almost 164 percent over 2020.

Here are the precise numbers for Group Death Benefits taken from Lincoln National’s annual statements for the three years:

2019: $500,888,808

2020: $547,940,260

2021: $1,445,350,949

Here are the key numbers for 2021, below, shown on the company’s annual statement that was filed with the Michigan Department of Insurance and Financial Services. These are national numbers, not state-specific:

Lincoln National is the fifth-largest life insurance company in the United States, according to BankRate, after New York Life, Northwestern Mutual, MetLife and Prudential.

The company was founded in Fort Wayne, Indiana in 1905, getting the OK from Abraham Lincoln’s son, Robert Todd Lincoln, to use his father’s name and likeness in its advertising.

It’s now based in Radnor, Pennsylvania.

The annual statements filed with the states do not show the number of claims — only the total dollar amount of claims paid.

Group life insurance policies, in most cases, cover working-age adults ages 18-64 whose employer includes life insurance as an employee benefit.

How many deaths are represented by the 163% increase? It is not possible to determine by the dollar figures on the statements.

But the average death benefit for employer-provided group life insurance, according to the Society for Human Resource Management, is one year’s salary.

If the average annual salary of people covered by group life insurance policies in the United States is $70,000, this may represent 20,647 deaths of working adults, covered by just this one insurance company. This would represent at least 10,000 more deaths than in a normal year for just this one company.

The statements for the three years also show a sizable increase in ordinary death benefits — those not paid out under group policies, but under individual life insurance policies.

In 2019, the baseline year, that number was $3.7 billion. In 2020, the year of the Covid-19 pandemic, it went up to $4 billion, but in 2021, the year in which the vaccine was administered to almost 260 million Americans, it went up to $5.3 billion.

The statements show that the total amount that Lincoln National paid out for all direct claims and benefits in 2021 was more than $28 billion, $6 billion more than in 2020, when it paid out a total of $22 billion, which was less than the $23 billion it paid out in 2019, the baseline year.

A $6 billion increase in expenses is something few companies could absorb, but Lincoln National has been working to do just that — by increasing sales of new insurance polices.

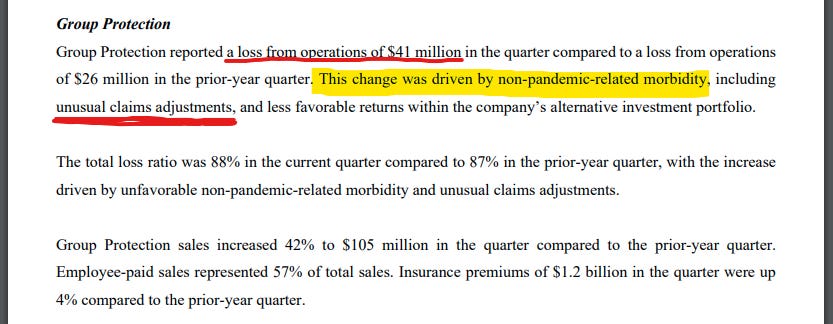

In the press release accompanying its annual report, and in its press release announcing the first quarter 2022 results — in which the company announces a $41 million loss in its Group Protection business — it trumpets an increase in sales. For first quarter 2022 that increase was 42 percent. The company also mentions that premiums have gone up 4 percent.

Interestingly, in the press release accompanying the first-quarter 2022 results, Lincoln National attributes the $41 million operating loss to “non-pandemic-related morbidity” and “unusual claims adjustments.”

“This change was driven by non-pandemic-related morbidity [emphasis added], including unusual claims adjustments [emphasis added], and less favorable returns within the company’s alternative investment portfolio.”

Morbidity, of course, means disease. A lot of people are sick.

This matches what I was told by OneAmerica in January in emails following the publication of my story in The Center Square — that it was not only deaths of working-age people that shot up to unheard-of levels in 2021, but also short- and long-term disability claims.

Annual statements for other insurance companies are still being compiled and reviewed. So far, Lincoln National shows the sharpest increases in death benefits paid out in 2021, though Prudential and Northwestern Mutual also show significant increases — increases much larger in 2021 than in 2020, indicating that the cure was worse than the disease — much worse.

Lincoln National’s stock price fell from about $70 a share on January 3 to $50 a share this week, and last month, a new CEO was installed. It doesn’t appear to be a sudden change, but could have been timed to assuage major shareholders who have no idea what’s really happening and may think that a fresh face and fresh ideas can turn this around. Could I suggest instead an honest and thorough assessment of what’s really driving these stunning numbers?

You must be logged in to post a comment.